After many hard lessons and tons of lost submissions, I have been collecting all this info for you and for future

reference for myself. We learn the same lessons over and over. So much to learn but even more to retain. Hit CTRL F and snoop around for your question(s). You may want to start from the bottom...gets better as you read. Some stuff may be outdated but still good to know.

reference for myself. We learn the same lessons over and over. So much to learn but even more to retain. Hit CTRL F and snoop around for your question(s). You may want to start from the bottom...gets better as you read. Some stuff may be outdated but still good to know.

MLO TIPS, TRICKS & LEGIT SHORTCUTS

1. On DURP ( DU REFI PLUS ) loans that require MI : DO yourself a favor and request your MI cert to be ordered right when your loan is approved or at least ask if it was requested. ( UWrs request these ) NOT PTD EITHER !!! So before you go and request a loan amount change, see if you can make the loan work as approved by changing your pricing to reduce cash out to zero. If a new MI cert is needed, 5-8 day turn times w/Radian...Maybe longer...read your DU!

2. Fannie Mae DU won’t take decimals in your loan amount, use round #'s in your LOS.

3. Get proof of self employment on your self employed borrowers ( Business License, Articles of Incorporation, LOE's from CPA ) ( See www.blackbook.com )

4. Scrub your final HUD and make sure it matches your Approval, Lock, payoff, anticipated closing date etc

5. Order Title & Escrow at loan disclosure stage when its an easy step to do.

6. When taking the 1003, request and add VOE info to your con-log for your JP/Processor.

7. Make sure you have all title fees INPUT prior to running DU and if expecting a DURP, no more than $250 cash back.

8. When getting GIFT FUNDS to close, make sure you have an "ACCEPTABLE DONOR" ( Search Fannie Guidebook ) Hint: for same sex unions, "Domestic Partner" is acceptable. Source the funds from the donor, source the wire and source leave the amount blank on the GIFT LETTER until you are ready to close.

9. Always use Title Profiles to furnish proof of property owned free & clear/ establish vesting/spellings etc.

10. Add the credit inquiry LOE to your needs list upfront.

11. DTI won't budge?,,,look at your credit card accounts... see if you have duplicates or accounts you can omit from the DTI ( Any auto loans with less than 10 months left etc?

12. Always scrub your bank statements for large deposits pre-submission. ( source ones that are > $1000 or 25% of gross income )

13. Always make sure your HUD's loan amount matches your loan approval and your credit/rebate is taken from the LOCK.

14. Always request AKA letters upfront IF you notice different name variations on your credit report. Look!!

15. Find a way of doing things or build a sales process that you know and feel good about and do it the same each and every time and leave yourself little crumbs along the way if you get lost.

16. Make sure the address on the signed 4506T is the same as what’s on your 1040's. ( Ask and look ) no computer generated signatures on 4506's...get real signatures!

17. Get LOE's on the multiple addresses, AKA's and inquires in last 120 days found on your credit report ( look and see )

18. On BofA and Wells Fargo ( Especially on your FHA Streamlines ) payoffs, be sure to net out your escrows PTD, ( Super Easy ) Less cash to close!! ...try to get to a zero HUD!

19. Date your loan disclosures the same date as your 1003.

20. Get or ask for the manual wire form from the bank or credit union when wiring money to escrow showing proof of where it came from. Make sure this account IS the one underwriting has and approved!!! Match up the #s!! IF not, make sure you get a gift letter from an acceptable donor and source the funds for the donor. HUGE issue if you fail this step. Always get this when wiring cash to escrow!

If you need cash to close make sure the borrower knows to write the check or wire the fund FROM the account your UWr has on file!!

21. Send out the two other FHA disclosures upfront in your Small Pack ( Energy Efficient Mortgage Doc and the Release of Liability disclosure )

22. Before you send out loan disclosures, make sure you have the correct spelling of names and middle initials etc. This is a 2 day time penalty and $80 in CA and $100 out of state fee to produce a new grant deed. Has to be drawn by attorney and a HUGE pain in the ACE!!

23. Get all bank statements that have transfers into your borrowers account and connect the dots. ALL!!

24. WHEN YOU HAVE A LOAN IN PROCESS FOR MORE THAN 60 DAYS, check your dates on your credit report and the PRELIM!!!. DONT REQUEST ALL THESE UPDATES @ CTC!!!...WATCH THE CLOCK! ask about our credit refreshes!! hope your brw didn't run up the revolving debt!

25. For FREDDIE MAC HARPS/ LP OPEN ACCESS check the new refinance Mortgage amount. It may not exceed the existing unpaid balance plus interest accrued through the date the mortgage is paid off, plus up to a maximum of the lesser of 4% of the current unpaid principal balance of the mortgage being refinanced or $5000 for related closing costs, financing costs and prepaids/escrows (actual costs only).

You cannot finance insurance premiums or tax installments that are currently due or past due

DO NOT ADD THE $75.00 PIW FEE OPEN ACCESS LOANS!!

26. Bank Of America Wires to close!!

I was informed by a client that Bank Of America has a wire cutoff time of 2pm PST for same day. ( WHAT? )

Yup… You would think that depository institutions can wire anytime. Not BofA!

My borrower went in to his branch and wired his funds ( BOOM! ) but they will post on Monday AM due to their cutoff times.

If you have any loans that are short to close and your borrower is opting to wire in the cash from a verified BofA acct, make sure they do this at least one day before your closing date ( they close @ 6pm on Fridays )

And give your cell number to confirm if a Saturday. The last thing you want is this to ruin your tier commissions. Protect the clock @ any cost!!

Make sure you let your brr know to use the reference # from Escrow too ! ( AKA Escrow # )

27. Gift of Equity can be used as down payment only. Cannot be applied towards closing fees and prepaids. However, a standard gift can be combined with the gift of equity if you are offering an FHA loan.

28. Re: Foreign Income

Foreign income (income generated from non-U.S. sources) may be used only if its stability and continuance can be verified, and is supported by U.S. Federal Tax Returns for the most recent two years. If the income is paid in a foreign currency the file must contain a printout evidencing the source used for the conversion of the foreign currency into U.S. dollars. The income must also be verified in the same manner as U.S. income sources

29. Revised large deposit Guideline ( now 50% not 25 %!! ) ( THIS MAY BE OLD as OF 8/15/2015 )!!!

Fannie revised this on 6/1

Large Deposits/New Accounts

Deposits into accounts may be an indication of recently opened liabilities, or an indication that funds used to cover closing costs, pre-paids, the down payment for purchase transactions, or reserves may be from an unacceptable source.

The source of funds must be explained and documented for the following:

1) An account opened within 90 days of application (i.e. funds used to open the new account) OR

2) A deposit, or the sum of unexplained deposits, on the borrower’s account statements required for the transaction, over a 30 day period of time that exceeds 25% of the borrower’s total monthly qualifying income for the loan.

Note: If the total of deposits meet the large deposit criteria as stated above, only the individual deposits within that total that exceed 10% must be verified

EXAMPLE 1

Mr. Borrower has a total monthly income of $10,000

There are 2 large deposits for $1,200

Since the aggregate is only $2,400 (24% of the total income) neither deposit needs to be verified

EXAMPLE 2

Mr. Borrower has a total monthly income of $10,000

There are deposits of $1,300, $1,100, $1,000, & $750

Since the aggregate is $4,150 (greater than 25%) the deposits greater than $1,000 (10%) must be verified ($1,300 and $1,100)

30. APR VS NOTE RATE ( TEXT BOOK ANSWER )

APR versus interest rate

When lenders advertise mortgage rates, they are required to display an additional number called the annual percentage rate, or APR.

The advertised rate is the one used to calculate your mortgage payment. Borrow $100,000 at five percent with a 30-year term, and the payment is $537. But an advertised rate tells you nothing about the cost of the loan or if it’s a good deal. Suppose you’re offered two loans. Both have a five percent rate, but one costs $1,000 and the other costs $4,000. They’re obviously not the same!

How is APR calculated?

In the example above, the payment for both loans is $537 per month. But because the first loan costs $1,000, you’re only actually getting $99,000 for that $537 monthly payment. When you pay $537 a month to borrow $99,000 the rate is 5.09 percent. The second loan costs $4,000, so for your $537 a month, you only get to borrow $96,000. In that case, the APR is 5.35%.

You don’t really need an APR calculation to tell you that the first loan is the better deal – it’s pretty obvious. But what if a five percent loan costs $1,000 but a 4.5 percent loan costs $4,000? Which is a better deal? That’s where APR comes in. The APR of the five percent loan in this case is 5.09 percent. The APR for the second loan is 4.85 percent. That means over the life of the loan, the second loan costs less than the first loan.

Is the loan with the lowest APR always the best?

Many people think that the loan with the lowest APR is automatically the best deal. That’s not true unless you keep your mortgage for its entire term. If not, the upfront costs of getting your mortgage are spread out over a shorter period of time, and that changes the true cost of the loan. Look at our two $100,000 30-year fixed loans again, but this time we’ll assume that you’ll sell the home in five years.

When you change the first loan’s term from 30 years to five years, its APR increases from 5.09 percent to 5.41 percent. And the second loan with its $4,000 in costs? It increases from 4.85 percent to 6.12 percent!

ARMs

Because no one can predict how interest rates will change over the years, the APR for adjustable-rate mortgages is calculated on the assumption that the loan is adjusting at that time. So if you have a 5/1 mortgage starting at three percent, and if it were adjusting today its rate would be six percent, that’s the rate used in the APR calculation. Even though it’s highly unlikely that rates in five years will be exactly what they are today.

The most important thing to remember when comparing APRs of ARMs is that they are calculated based on current economic conditions. The APR of a loan on Monday may be different from the APR of that same loan on Friday. You need to get your mortgage quotes on the same day (preferably at the same time). This is easiest to manage by getting your quotes online. Remember this ( IPL ) All Arms have adjustment periods, I is for Initial, P is for Periodic, L is for liftime adjustment. Capps are going to be more than likely 2/2/5 or 5/2/5. I/P/L...same place slots man!!! 2/I,2P,/L5...

30. VA & FHA Case # Transfers? Check the forms page on this site. There is a template that you can edit ( plug & play ) done deal! Use it and fax to the lender that currently holds the case #.

31. RETIREMENT FUNDS & PENSIONS?? If you have a pension based income, request the 3 yrs continuance ahead of time!!!!! Sometimes the 3rd party will only mail them. I had one the took 5 to 7 days to mail out. Order them early! Some borrowers have them.

Always request the 3 yrs. continuance on any income that isn't W2/paycheck.

32. If you plan to originate a VA LOAN and need a termite inspection report ( FORM 33 ) , request that the report be filled out with the following verbiage.

REQUIRED VERBIAGE ON ALL TERMITE REPORTS AS FOLLOWS:

Termite Inspector Verbiage

"This is to certify that the above property was inspected on (date of inspection) in accordance with the Structural Pest Control Act and rules and regulations adopted pursuant there to, and that no evidence of active infestation or infection was found in the visible, accessible areas."

Borrower Verbiage

Clearance Section: "The recommendations in this report have been completed to my satisfaction at no expense to me."

33. Ask IF the borrower EVER received a loan mod! ( Considered just like a Short sale.) Seven years out from date of modification. This guideline will more than likely change for the better.

34. Foreclosures, Short sales FHA RULES A borrower whose previous residence or other real property was

foreclosed on or has given a deed-in-lieu of foreclosure within the previous three years is generally not

eligible. FHA considers a borrower to be eligible to refi / buy 2 yrs after the discharge of a CH 7 or CH 13 Bankruptcy.

35. Whenever you have a borrower that has more than one home, always look at the 1040 or the drivers license ( VA & FHA ) for their address. I had one when the borrowers had moved out and moved into anew home but back into their old home which is now our subject property. this is fine but along the way, the wife and the husband got drivers licenses and SSN cards to read the old addresses. They have since moved back into our subject. This is fine, BUT get an LOE, and Utility bills upfront so the UWr knows what the heck is going on. Occupancy issues.

36. For FHA Streamlines you need a net tangible benefit of at least 5% monthly savings. The way this means test is calculated is by taking your current MMIP and principle and interest payment and multiplying by .05%. ( Example: $1525 P&I, $235 MMIP =$1760.00 per month ( $1760 X .05 = $88.00) your new payment needs to be $88.00 per month lower that this amount. Or easier stated $1672.00 or less.

If you have an old FHA loan from before May 2009, you should be either @ .50 of .55% MMIP. You can rest assured you mean the means test. If you loan was endorsed after May 31 2009, your MMIP will go up to 1.250 or 1.25%. Run these numbers then. If you have an old one and need to loon up the historical FHA MMIP chart, click here!

37. Home was previous listed and now wants to refi. Get the listing cancellation agreement. Date your 1003 after that date!! IF the borrower did a cash out refi with on the previous SIX months, you are good to go! If not, they must wait. IF you have a regular old refi. Make sure the BRRs cancel the listing and get the List cancellation document. You must get an LOE about why they cancelled it and then date the 1003 and pull credit after that date!!!!! ( make sure you quote the extra fees for the extra forms for a rental!! ( You need forms 1007 and 216 ) Make sure your GFE discloses these fees!!

38. In order for an amended tax return transcript to be pulled, it needs to be specified on the request ( 4506-T ),

(they will not automatically pull the most recent ones); please see below & have your PA order the amended returns for your file. On the 4506T we must check box 6b and on the order form under service requested we must type “amended” or the IRS will send the original request. ( this sucks but it is what it is like most rules. ( IRS, 4506 )

39. Temporary Leave, Short Term Disability and Maternity Income

Below are the guidelines for Short term disability and Maternity Leave

Both Fannie Mae and Freddie Mac have issued new policy with regards to Temporary Leave Income. As such, Citi’s Family Medical Leave of Absence policy has been renamed Temporary Leave Income and the new policies now

address when income from their “leave of absence” position may be used to qualify and how to calculate qualifying income.

Income used to qualify is determined by when the borrower will be returning to work:

If the borrower will return to work prior to the first mortgage payment being due, the borrower’s regular employment income that will be received upon their return to employment can be used to qualify.

If the borrower will not return to work prior to the first mortgage payment being due, the lesser of the borrower’s temporary leave income (if any) or their regular employment income may be used to qualify. If the borrower will not return to work prior to the first mortgage payment being due and the borrower’s temporary income is less than their regular pay, liquid assets may be used to supplement the temporary leave income.

40.As many of you are already aware, updated loan limits have been announced for 2013. Please see below for program specific details.

Conventional Loan Limits:

The FHFA recently announced that the Conventional Conforming loan limits will remain at existing levels in

2013.

Conventional Conforming loan limits are published by FHFA at:http://www.fhfa.gov/Default.aspx?Page=185

VA Loan Limits:

VA has posted new, county specific, loan limits for 2013, for VA Jumbo loans (loan amounts above

$417,000).33 county loan limits will increase, 63 county loan limits will decrease, and 46 will remain the same.

VA loan limits are published by VA at:

http://www.benefits.va.gov/homeloans/purchaseco_loan_limits.asp

The new VA loan limits are effective for loans with note dates on, or after, Tuesday, January 1, 2013.

FHA High Balance

FHA has announced that the floor and ceiling loan limits will remain the same. The 1-unit property minimum (floor) currently stands at $271,050, and the maximum (ceiling) stands at $729,750.

These levels will remain unchanged. Counties with limits that fall between the floor and the ceiling may have changed. Please refer to HUD’s website for details on particular counties.

HUD loan limits are published here:https://entp.hud.gov/idapp/html/hicostlook.cfm

The new FHA loan limits are effective for loans with case numbers issued on, or after, Tuesday, January 1, 2013.

41. On FHA STREAMLINES: Don't try to submit a loan that was an old 15 yr unless you have a 20 yr option.

I have a deal now that was an old 15 yr and the borrower wants to streamline to a 30 yr. Looks good, sounds and pencils out nicely. DONT DO IT!!! //////

FHA has this weird random a$$ rule that prohibits a borrower adding more than 12 yrs. to the life of their FHA loan. So, in my case I had a guy that got an old FHA loan in 2008 ( same MIP and .10 UFMIP )... The borrower has 12 yrs left on a 15 yr. loan The maximum is I can do a 22 yr. loan. Since we don't offer a 22 yr, the next best thing is a 20 yr or another dang 15 which has not much benefit anyhow. Applies to the regular FHA product too! Cant add more than 12 yrs to the new loan...PERIOD!!

42. Additional borrowers may be added to the DU Refi Plus as long as the original borrowers on the loan being refinanced are retained.

· A borrower who is on the original loan being refinanced may be excluded from the

DU Refi Plus only when the following requirements are met:

· The remaining borrower must provide evidence that he or she has been making the payments on the existing mortgage from his or her own funds for the most recent 12months prior to the origination of the new mortgage (the 12-month payment history must be on the existing mortgage).

43. With regards to Texas refinance loans, you know that random “extension of credit disclosure” in the small package?

I have one that started out as a non cash out ( Brr didn’t know ) title came in and was flipped it to a cash out 50

(a ) ( 6 ),TEXAS CASHOUT mid-stream.

#1 Add $150 to the attorney fee for the COC and make sure the fee is added to the GFE!!

#2 Make sure the non borrowing spouse signs and dates this "extension of credit document" 12 calendar days prior to closing and gets uploaded for the CTC.....This will kick your CTC request out and you will have to wait for 12 long days

44. Second Homes ( Citi )

A second home is defined as 1-unit property (including condominiums, co-ops, and PUDs), unless otherwise indicated in a process or program fact sheet, that the borrower occupies for some portion of the year in addition to their principal residence. A borrower may have more than one second home. Often located in a vacation/resort area, although not always, the property must be suitable for year round occupancy. A second home should not be in the same market as the borrower's primary residence.

However, there are exceptions, such as:

• Property located in a recreational area which is part of a metropolitan area (e.g., beach house), or

• Property used to minimize commuting problems (e.g., a Manhattan condominium owned by a Connecticut resident working in New York City).There are no specific mileage requirements with regards to the distance between the primary and second home. Good judgment must prevail.

• Rental income may not be used to offset the expense of a second home. ( check your 1040's for rental income! )

• 2-4 unit property is not eligible as a second home, except DU Refi Plus and Fannie Mae Refi Plus. Refer to the DU Refi Plus fact sheets for availability and additional details.

• There may not be an occupant besides the borrower that resides in the subject property, and the borrower must retain exclusive control over the property. The sales contract or appraisal must not reflect that there are timeshare arrangements or any other rental agreements that requires the property to be rented. The borrower may not give management firm control over the occupancy of the property. Transactions where the property is being purchased for the occupancy by someone other than the borrower must be registered and underwritten as an investment property.

45. BANK OF AMERICA WILL NOT REFI A HARP ELIGIBLE LOAN THAT ISNT THEIR OWN!

I found this out while taking a loan app for a BofA employee! ( go figure )

46. Employment GAPS ? You must get and submit a letter to explain why and IF its recent, also request the new paystubs. You/We cant fund and record ( Fannie Overlay ) without have 30 days pay stubs so make sure you have these and if you don't, set the expectation upfront that their loan WILL NOT FUND until they receive their 30 day pay stub!! And IF they are having second thoughts on their new job, let them know that they MUST stay employed there for at least 90 days AFTER we close. Once we sell the loan to an investor, at times they also check the VOEs!!!

47. You know when your value comes in higher ( happens every now and then ) on loans where you sent it out @ 62% LTV or 77% LTV? I call em threshold LLPA deals. Make sure that when value comes in that you re-run your pricing to make sure you get the credit to the client to use for fees or drop the rate .125%!! By law, the HOUSE cannot let you participate in the added rev either!!! be on your game! If your company archives rate sheets in your LOS like mine, go back and re-run the #'s!! On the flip side, also be aware that value oftentimes come back short. Run the #'s, inform/sell the client of the changes or request a pricing exception to off set this adjustment! ( upload email communication to your BRW for the COC re-disclosure.

48. Assets, assets and elbows!

Anytime you have a subject/ investment property, you need assets! EACH investment home or 2nd home, you need 6 mos PITI and IF the loan you are stacking(packageing for submission ) you need an additional 2 mos PITI for that home!! For 401K accounts use 60% of the balance and the terms of withdrawal or get individual not business cash bank statements or gets IRA's CD s ect///Anything with cash in their name!

49. Need SSI Award Letters for your retirees/permanently disabled borrowers?

Here is the link for your borrower to get a copy of their social security award letter:

http://www.ssa.gov/myaccount/

and here is where they would login or set up an account:

https://secure.ssa.gov/RIL/SiView.do

They will be able to get it right online via the automated system.

50. This tip comes from Chris Sutherland, DSM/Paramount Equity.

If the borrower doesn't impound, we will require their insurance to be paid through 12 months. If they do impound, all we need is 3 months collected.

51. This is a TIP that probably doesn't get as much credit as it needs. When you have a FHA "A" borrower or standard FHA loan on the deck, REQUEST THE CASE # ASAP!!...this race has two legs. The first race is who get's the case # issued 1st!! ...The second race is who gets the client docs back along with disclosures. It's not always about the lowest rate!

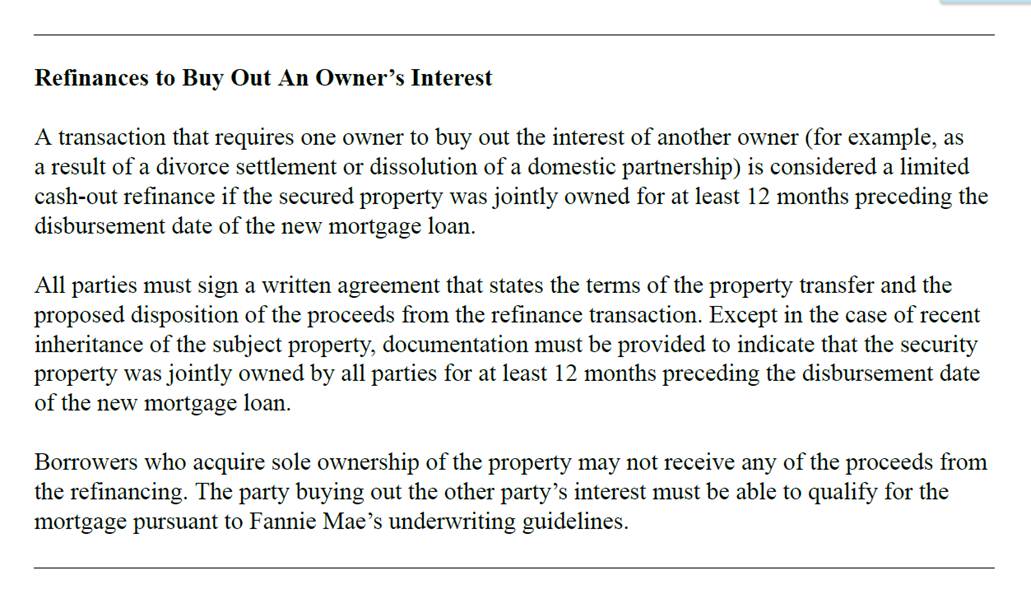

52. ( Shot-Out to Mike Reilly of PEM direct on this one )

I don’t see this often but I wanted to share something that can hopefully pick up a deal here and there. Scenario – borrowers are married and getting divorced. One party needs to “buy out” the interest of the other. Let’s assume our borrower needs to pay the soon to be x-husband/wife 50K (per the divorce decree.) We want to pay off the existing mortgage(s) plus give the x-husband/wife $50K.

Question(s)

Is this a cash out or rate and term refi?

What LTV can you go to?

Is this the same for Conv and FHA?

Answers

This would be considered Rate and Term for both Conv and FHA

You can go to max RT LTV (FHA would be 97.75 and Conv is 95, soon to be 97 when DU updates)

You are ok to go to 97.75 and call it a R/T. I would cut and paste this guideline in the milestone comments or a processor cert just so the UW knows.

https://www.fanniemae.com/content/guide/sel110315.pdf

53. FHA Flips The buyers app must be 91 days after acquisition date! ( Pull a property Profile 1st !! )

54. Non Permitted Room Additions got you all twisted up? I had one where it was an enclosed patio that was done right but no PERMITS!!! read this below, It will help: ( Shot out to Manger/MLO Doug Locsin out there )

General guidance on this issue from Santa Ana HOC:

· Needs to be separated out on the sketch so we can see where it is and how it attaches (also access) to the home.

· Should be a line item on the grid for the addition or any comments on its 1) contributory value or lack of, 2) the marketability of the property with the addition, and 3) if any of the comparables have similar permitted and non-permitted additions (and those should be identified in the grid with the appropriate adjustment if one is warranted.

· Appraiser to comment on the addition and whether or not it was completed in a workmanlike manner.

** This is from the new HUD handbook.

iii. Additions and Converted Space

The Appraiser must treat room additions and garage conversions as part of the GLA of the dwelling, provided that the addition or conversion space:

• is accessible from the interior of the main dwelling in a functional manner;

• has a permanent and sufficient heat source; and

• was built in keeping with the design, appeal, and quality of construction of the main dwelling.

Room additions and garage conversions that do not meet the criteria listed above are to be addressed as a separate line item in the sales grid, not in the GLA. The Appraiser must address the impact of inferior quality garage conversions and room additions on marketability as well as Contributory Value, if any.

The Appraiser must analyze and report differences in functional utility when selecting comparable properties of similar total GLA that do not include converted living space. If the Appraiser chooses to include converted living spaces as GLA, the Appraiser must include an explanation detailing the composition of the GLA reported for the comparable sales, functional utility of the subject and comparable properties, and market reaction.

Alternatively, the Appraiser may consider and analyze converted living spaces on a separate line within the sales comparison grid including the functional utility line in order to demonstrate market reaction.

The Appraiser must not add an ADU or secondary living area to the GLA.

{kind=link}