VA LOANS

VA loans are solid loans if and when you have them.

Can you remove the Co-applicant from the loan? As long as they are on the NOTE, NO! ( unless there was a divorce or death )

90% MAX cash out!! ) NO PMI!!

100% on purchase loans

Need termite report and COE ( see forms ) ( All VA Loans require a COE ) request @ loan registration step.

100% Max IRRRL ( 2055 Appraisal! ) Drive by with value ( $ 250 )

Wells Fargo to Wells Fargo = Needs no appraisal at all!! ( Like a FHA Streamline )

IRRRLs can't flip to 15 from 30 though!

Funding fees can be a PITA though. On small loan amounts, flip to Lender paid of need be

Ask if they are eligible for a Funding Fee Waiver ( must be 10% or more dissabled though )

VA Loan Funding Fees VA Loan Guidelines

Note: For Loans Closed on or After November 22, 2011

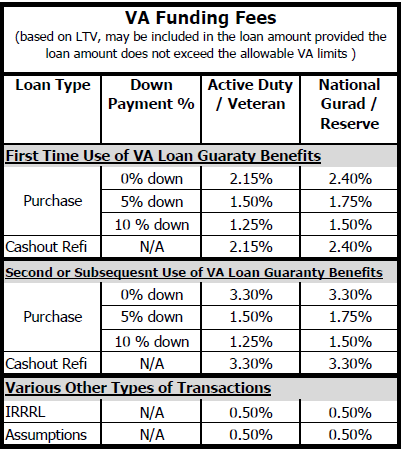

The VA funding fee is required by law. The fee, currently 2.15% on no down payment loans for a first-time use, is intended to enable the veteran who obtains a VA home loan to contribute toward the cost of this benefit, and thereby reduce the cost to taxpayers. The funding fee for second time users who do not make a down payment is 3.3%. The idea of a higher fee for second time use is based on the fact that these veterans have already had a chance to use the benefit once, and also that prior users have had time to accumulate equity or save money towards a down payment.

For purchase and construction loans, members of the regular military fall into the category of first time user or subsequent user. For first time users, no down payment requires a 2.15% fee, down payment of at least 5 percent but less than 10 percent requires a 1.5% fee, and down payment of 10% or more requires a 1.25% fee. For subsequent users, no down payment requires a 3.3% fee, down payment of at least 5 percent but less than 10 percent requires a 1.5% fee, and down payment of 10% or more requires a 1.25% fee.

For the category of Reserves / National Guard, first time users with no down payment requires a 2.4% fee, down payment of at least 5 percent but less than 10 percent requires a 1.75% fee, and down payment of 10% or more requires a 1.5% fee. For subsequent users for the category of Reserves / National Guard, no down payment requires a 3.3% fee, down payment of at least 5 percent but less than 10 percent requires a 1.75% fee, and down payment of 10% or more requires a 1.5% fee.

Cash-out refinancing loans for regular military require a 2.15% fee for first time users and a 3.3% fee for subsequent users. For Reserves / National Guard, the requirement is a 2.4% fee for first time users and a 3.3% fee for subsequent users. If there are down payments involved, refer to the information above.

On interest rate reduction loans( IRRRLS), the VA funding fee is .50% and it is 1.0% on Manufactured Home Loans.

The following persons are exempt from paying the funding fee:

- Veterans receiving VA compensation for service-connected disabilities.

- Veterans who would be entitled to receive compensation for service-connected disabilities if they did not receive retirement pay.

- Surviving spouses of veterans who died in service or from service-connected disabilities (whether or not such surviving spouses are veterans with their own entitlement and whether or not they are using their own entitlement on the loan).

VA Loan Limits

VA has posted new, county specific, loan limits for 2013, for VA Jumbo loans (loan amounts above $417,000).

33 county loan limits will increase, 63 county loan limits will decrease, and 46 will remain the same.

VA loan limits are published by VA at:

http://www.benefits.va.gov/homeloans/purchaseco_loan_limits.asp

The new VA loan limits are effective for loans with note dates on, or after, Tuesday, January 1, 2013.

TIP!!

Hey guys for your people. VA Benefits letter website.

https://www.ebenefits.va.gov/ebenefits-portal/ebenefits.portal

*******VA Certificate Of Eligibility Request Hotline*************

Just call this # 888-869-0194 ext 3048 and be polite!

IRRRL Facts

- No appraisal or credit underwriting package is required when applying for an

IRRRL. - An IRRRL may be done with "no money out of pocket" by including all costs in

the new loan or by making the new loan at an interest rate high enough to enable

the lender to pay the costs. - When refinancing from an existing VA ARM loan to a fixed rate loan, the

interest rate may increase. - No lender is required to give you an IRRRL, however, any VA lender of your

choosing may process your application for an IRRRL. - Veterans are strongly urged to contact several lenders because terms may

vary. - You may NOT receive any cash from the loan proceeds.

Eligibility

An IRRRL can only be made to refinance a property on which you have already

used your VA loan eligibility. It must be a VA to VA refinance, and it will

reuse the entitlement you originally used.

Additionally:

- A Certificate of Eligibility (COE) is not required. If you have your

Certificate of Eligibility, take it to the lender to show the prior use of your

entitlement. - No loan other than the existing VA loan may be paid from the proceeds of an

IRRRL. If you have a second mortgage, the holder must agree to subordinate that

lien so that your new VA loan will be a first mortgage. - You may have used your entitlement by obtaining a VA loan when you bought

your house, or by substituting your eligibility for that of the seller, if you

assumed the loan. - The occupancy requirement for an IRRRL is different from other VA loans. For

an IRRRL you need only certify that you previously occupied the

home.

Applying for a VA Loan After a Short Sale

A frequently asked question about VA home loans has to do with how long a borrower must wait after a short sale before the person is eligible to apply for a new VA mortgage loan. The standard answer? VA regulations stipulate a two year waiting period following the short sale before a borrower can be considered for a new VA mortgage.

But some situations are unique-what happens when a borrower is involved in a short sale two years prior to applying for the new VA loan, but any remaining amount on the loan still owed isn't paid off until much later?

In these cases, much depends on the lender. Some lenders would deny the loan in this circumstance. But other lenders--like me--do work with borrowers in circumstances similar to this, allowing a new VA loan application if certain conditions are met.

To be approved for the new VA home loan, the borrower would have to maintain good credit after the short sale, and the date of the short sale must be documented on a credit report or other paperwork.

In cases where the lender approves of the new loan, the VA loan applicant who has good credit, has waited two years since the official date of the short sale, and provides the required supporting evidence could be approved for a new VA home loan.

It's important to point out that not all lenders permit these types of transactions, and some require the borrower to wait longer than the VA two year minimum. But lenders who do agree can help a qualified borrower ready to become a homeowner again--even after a short sale.

When a VA borrower starts having trouble making VA mortgage loan payments, sometimes the only alternative to foreclosure is a short sale-a transaction where the borrower agrees to sell for less than the property is worth (or was worth when the housing market was more favorable), or less than is what is actually owed on the property.

The short sale is a last resort in many cases, but if foreclosure seems unavoidable it may be the best option. After all, a borrower has the right to sell the home at any point during the foreclosure process. This option is available as long as the borrower still legally owns the home.

Short sales sometimes involve something called the VA compromise claim. According to the VA official site, "If your property cannot be sold for an amount which is greater than or equal to what you owe on the loan, VA may pay a "compromise claim" for the difference to help you complete the sale. You must contact VA to discuss the situation and get prior approval for a sale with a compromise claim payment. Some mortgage companies are authorized by VA to approve a sale with a compromise claim."

Avoiding foreclosure by using a short sale does affect a credit rating; unfortunately short sales lower credit scores in many cases, and there is usually a "seasoning period" borrowers must wait out before they are allowed to apply for another home loan.

The good news is that a seasoning or waiting period for VA loan borrowers may not be as long as for conventional borrowers in similar circumstances. Some lenders--but not all--require a three-year waiting period between the time of a short sale and a new loan application.

I only a two year waiting period cases-if the borrower has a history of good credit since the short sale and a qualifying credit score, a 24 month wait may be all that's required. Credit and payment behavior post short sale are very important factors in deciding if a borrower can apply again after only a two-year wait.

If you had a VA insured loan in the past, experienced financial trouble, and needed to resort to a short sale, you are not locked out of the housing market.

Appraisals

When requesting a VA appraisal, please complete this VA form. If the appraisal request is for a purchase transaction, the purchase contract along with any applicable counters-if available, should also be sent with the 26-1805. If you have any questions, let me know.

****A Construction to Permanent financing mortgage may be closed as a purchase money transaction, limited cash out refinance, or cash out refinance transaction. When a refinance transaction is used, the borrower must have held legal title to the lot before they applied for the construction financing and must be named as the borrower for the construction loan.

The method for determining the LTV will vary based on the type of transaction and the length of time the borrower has held legal title to the lot; and in some cases, how title was acquired.

Purchase: When a purchase money transaction is used and the borrower acquired the lot greater than 12 months prior to the application date of the construction loan, or if the borrower acquired the lot through an inheritance or gift (regardless of the date of acquisition), the LTV is determined by dividing the loan amount by the lesser of:

· The current appraised value of the lot and improvements, or

· The sum of the documented construction costs plus the current appraised value of the lot.

If the borrower acquired the lot less than 12 months prior to the date of the construction loan application, the LTV is determined by dividing the loan amount by the lesser of:

· The current appraised value of the lot and improvements, or

· The total acquisition costs (the cost of the improvements plus the cost of the lot as documented by a copy of the purchase contract, fully executed HUD1 settlement statement, or appraisal report).

Refinance: When limited cash out or cash out refinance transaction is used; the borrower must have acquired title to the lot prior to applying for construction financing and must be named as the borrower on the construction loan.

If the borrower acquired the lot more than 12 months prior to the date of application for the construction loan, the LTV is determined by dividing the loan amount by the current appraised value of the lot and improvements.

If the borrower acquired the lot less than 12 months prior to the date of the construction loan application, the LTV is determined by dividing the loan amount by the lesser of:

· The current appraised value of the lot and improvements, or

· The total acquisition costs (the cost of the improvements plus the cost of the lot as documented by a copy of the purchase contract or fully executed HUD1 settlement statement.

Assumable Construction Financing

Citi will purchase conventional conforming loans that were originated in the builder or seller's name and subsequently assumed by the borrower subject to all the following:

· Purchase money transactions only. LTV/CLTV requirements defined by the product and documentation process selected.

· The age of income and asset documentation used to qualify the borrower may not be more than 180 days old at the time the assumption loan was closed.

· A new full appraisal obtained at the time of borrower purchase is required.

· The borrower may not be an affiliate of the builder, developer or seller of the property.

· The original loan amount, prior to the borrower's assumption, is limited to conforming loan sizes only.

The Citi Assumption Agreement (found in the Exhibits section) should be used when delivering a loan to Citi where the borrower has assumed the construction loan.

VA Loan Fact SheetDefinition, Features, and FactsWhat is a VA Guaranteed Loan?

VA guaranteed loans are made by private lenders, such as banks, savings & loans, or mortgage companies to eligible veterans for the purchase of a home which must be for their own personal occupancy. To get a loan, a veteran must apply to a lender. If the loan is approved, VA will guarantee a portion of it to the lender. This guaranty protects the lender against loss up to the amount guaranteed and allows a veteran to obtain favorable financing terms.

There is no maximum VA loan but lenders will generally limit VA loans to $417,000. This is because lenders sell VA loans in the secondary market, which currently places a $417,000 limit on the loans. For loans up to this amount, it is usually possible for qualified veterans to obtain no down payment financing. A veteran's maximum entitlement is $36,000 (or up to $104,250 for certain loans over $144,000). Lenders will generally loan up to 4 times a veteran's available entitlement without a down payment, provided the veteran is income and credit qualified and the property appraises for the asking price.

VA Loans Offer the Following Important Features:

- Equal opportunity for all qualified veterans to obtain a VA loan.

- No down payment (unless required by the lender or the purchase price is more than the reasonable value of the property).

- Buyer informed of reasonable value.

- Negotiable interest rate.

- Ability to finance the VA funding fee (plus reduced funding fees with a down payment of at least 5% and exemption for veterans receiving VA compensation).

- Closing costs are comparable with other financing types (and may be lower).

- No mortgage insurance premiums.

- An assumable mortgage.

- Right to prepay without penalty.

- For homes inspected by VA during construction, a warranty from builder and assistance from VA to obtain cooperation of builder.

- VA assistance to veteran borrowers in default due to temporary financial difficulty.

- Guarantee that a home is free of defects. VA guarantees only the loan. It is the veteran's responsibility to assure that he/she is satisfied with the property being purchased. The VA appraisal is not intended to be an "inspection" of the property. A veteran should seek expert advice (a qualified residential inspection service), as necessary, BEFORE legally committing to a purchase agreement.

- If you have a home built, VA cannot compel the builder to correct construction defects although VA does have the authority to suspend a builder from further participation in the home loan program.

- VA cannot guarantee that a veteran is making a good investment.

- VA cannot provide a veteran with legal services.

- Contract to purchase: Veteran selects home and discusses purchase with seller or selling agent and signs purchase contract conditioned on approval of a VA guaranteed loan.

- Loan application: Veteran selects lender, presents Certificate of Eligibility, and completes loan application. Lender will develop all credit information and request VA to assign a licensed appraiser to determine the reasonable value for the property. Veteran will pay for credit report and appraisal unless the seller agrees to pay. Either VA or the lender will issue a value for property for loan purposes based on the appraisal.

- Loan decision: If the established value is acceptable to all parties and the lender develops that a veteran is credit and income qualified, the loan may be approved. Most lenders are authorized to make this decision.

- Loan closing: Veteran (and spouse) attend the loan closing and sign the note, mortgage, and other related papers. The lender or closing attorney will explain the loan terms and requirements as well as where and how to make the monthly payments. When the loan is reported to VA, the Certificate of Eligibility is annotated to reflect the use of entitlement and returned to the applicant. (The loan closing procedure may vary in some states.)